Respected Pradhan Mantriji

RE: PRIME MINISTER JAN DHAN YOJANA

You have today launched massive and ambitious PRIME MINISTER JAN DHAN YOJANA programme under financial inclusion with an object to provide banking facility to those who do not have bank accounts at present. The target fixed under the programme is to open 7.5 crores bank accounts within period of one year starting from 15th August, 2014. I wish to congratulate and compliment you for taking such a bold initiative to connect 7.5 crores households with the economic activity and prosperity of the country and remove “Financial Untouchability” from the country. As per the announcement made by you while inaugurating the programme in Delhi, on first day itself 1.5 crores new accounts have been opened under the programme and you have set the target to open balance 6.5 crores accounts by 26th January,2015 itself instead of waiting for next independence day.

2. On the basis of communications issued by the government and RBI and news items appearing in the media on the subject, the main features of the scheme are as under

FEATURES

(a) Target group is those households who do not have bank accounts at present and belonging to poor section.

(b) Bank accounts will be opened without much hassle and formality. RBI has issued guidelines to banks that KYC norms may be exempted for first 6 months for opening such accounts with maximum turnover of Rs. One lakh and balance in the account should not be more than Rs. 50,000 at any time.

(c) The account holder will be entitled to receive “RuPay” DEBIT CARD issued by National Payment Corporation of India simultaneously with opening of the account from day one FREE OF COST.

(d) The account holders will be automatically covered for accident insurance up to Rs. One lakh under the policy issued by HDFC FREE OF COST EVERY YEAR.

(e) In addition of the above, those who open accounts under the scheme by 26.01.2015 will be entitled to receive automatic life cover of Rs. 30,000 under the policy issued by Life Insurance Corporation of India FREE OF COST.

(f) Account holder will be eligible to receive overdraft facility of Rs. 5000 after 6

months of opening the bank account ON AUTOMATIC BASIS.

These are highly attractive and beneficial features for the common man which not only get modern and high tech banking facility but also get life and accident insurance cover. It is big social net to the poor.

3. However I strongly feel that to make the scheme

successful and sustainable, the following issues need

to be addressed immediately.

(a) COST FACTOR: Huge cost will be involved for implementation of this programme. New 7.5 crores to be opened will be more or less equivalent to 20 percent of existing deposit accounts being handled by the banking system of the country. I feel most of the accounts to be opened initially will be with ZERO balance.

The following 4 agencies in addition to government of India and RBI namely ( i ) Banks (ii) National Payment Corporation of India for issuing RuPay Debit Card (iii) HDFC Aro for issuing accident policy and settlement of claims (iv) LIC for issuing life cover and settlement of claims will be responsible for successful implementation.

Total insurance cover to be provided for 7.5 crores accounts under the scheme will be as under

(a) ACCIDENT INSURANCE COVER ONE LAKH x 7.5 CRORES 7.5 LAKH CRORES

(b) LIFE COVER 30,000 X 7.5 CRORES 2.25 LAKH CRORES

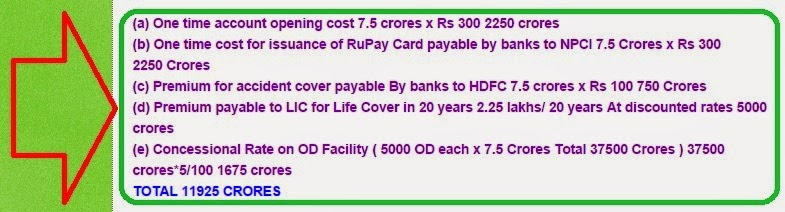

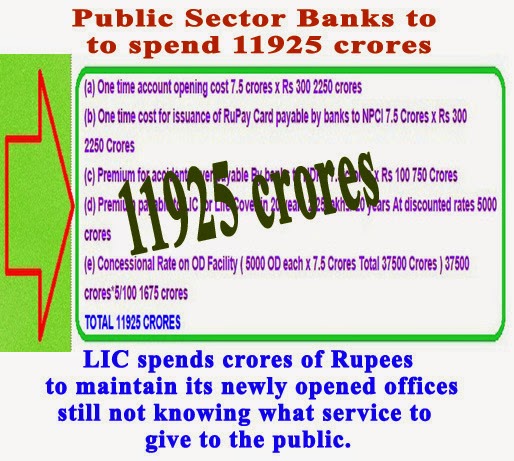

I presume the following cost for implementation of the scheme to achieve the target in the given time frame work

I understand that this cost incurred for implementation of the scheme will be borne by the government. But, initially payments will have to be made by banks and then reimbursements will be given to banks.

As you know public sector banks are already passing through severe profitability constraints. Such a huge expense burden will put further pressure on profitability front and will create further negative perception about PSU banks functioning among investors. I therefore suggest that claims for expenses incurred by different agencies in this regard may be directly settled by the government instead of bank settling first and then claiming reimbursement.

(2) COORDINATION AMONG DIFFERENT AGENCIES

5/6 different agencies will be responsible for implementation of the scheme while contact point for account holders and final delivery of the product will be at bank counters. Therefore it is very necessary that there should be perfect coordination among different agencies at all levels right from opening of accounts, delivery of debit card, mobile services , settlement of insurance cover etc to make it successful. In the absence of this, blame game can start among the implementing agencies derailing it earlier than expected.

(3) PROCEDURE HASSLES

(3) PROCEDURE HASSLESProcedure details need to be codified and documented immediately. Anxiety for speedy

implementation of the project can be well understood and appreciated but to open one and half crores accounts in single day and to further open 6.5 crores accounts in next 5/6 months without detailed procedure instructions to the operating staff can come as boomerang on the scheme in coming days and create serious question mark on its creditability as has happened on many schemes in the past. Some of the illustrations in this regard are given below

- (a) Presently, RBI has permitted opening of account only with production of photo and signature in the presence of bank officials without following normal KYC norms immediately and the same can be completed later on within maximum period of 6 months. Now, it should be clarified and instructions to be given as to what will happen after 6 months in case the account holder fail to comply KYC norms. Such cases are going to be large as the targeted group is less educated and migrating folk. Whether such accounts will receive fate of closer. You have shared your experience that Dena Bank officials chased you for 20 years for closer of your deposit account. You want that this programme should be for opening more and more bank accounts rather than closing of accounts after some time.

- (b) It is proposed that OD facility will be granted after 6 months of opening of the account subject to its satisfactory conduct. Most of these accounts will be opened with zero balance and either with no operation or with very limited operations in first 6 months in the absence of any credit facility. It should be immediately clarified that what will be norms for treating the account satisfactorily conducted. It should not be entirely left to the discretion of the operating staff. What will be procedure for grant of OD - whether on automatic basis or whether it will call for completion of paper work and documentation. Now all account holders have carried the impression that OD facility will be available to them from banks. In case the ratio of refusal goes high because of norms fixed or due to perception of bank officials, it will create huge dissatisfaction to the account holders.

- (c) Claim settlement procedure at LIC and HDFC need to be immediately codified and documented to avoid future dissatisfaction among the account holders. The procedure need to be advertised. In case of LIC what will be the cooling for lodgment of claim after opening of the account. Proper authorities should be created for settlement of such claims.

- (d) Banks have been given task of opening 7.5 crores new accounts in next 6 months. It is huge huge workload on the staff which are already overburdened due to staff shortage and increasing business and ever-increasing variety of products. Further the bank staff is at present highly de-motivated due to very poor payments compared to the much better service conditions prevailing in private banks and in the government sector. I have to draw your attention that wage negotiation for bank employees is pending for last 2 years without any finality. Govt./ IBA are sitting tight on it without any development. Such scenario is becoming frustrating for bank employees and fails to attract talent in the industry. How do you expect that under such conditions the programme will become successful at the bank level which is the most critical point for it. I therefore urge you immediately intervene in the matter and sanction attractive package to them.

- (e) The private sector banks should also be called upon to participate in this national programme of removal of financial untouchability. Today private sector banks control about 25 percent of total bank business. They should be asked to share at least proportionate responsibility and implementation of social programme should not be responsibility of PSU banks alone.

I hope my above suggestions will receive your attention and appropriate action will be taken wherever felt necessary. I wish all success in your endeavor.

With Respectful Regards

Yours Sincerely

SHARBAT CHAND JAIN, FORMER GENERAL MANAGER, BANK OF INDIA

D/1/1 SECTOR C SCHEME NO 71, INDORE 71 ( M.P. ) 452009 Mobil No 08966019488 Email sharbat_123@rediffmail.com

Date 28.08.2014